With all the people, paperwork and time-intensive steps involved, getting a mortgage can seem a little like running an obstacle course.

But if you take the time to understand the homebuying process and come to it with a strong sense of your own finances, you can hurdle, balance and sprint your way around the course without a scratch.

Before the housing crisis of 2008–09, it seemed that anybody could get a mortgage. Lenders pushed “sub-prime” loans on people with poor credit knowing the entire time that the applicants couldn’t afford the payments and would eventually default. These lending habits were obviously unsustainable, and we know the rest of the story. The banks got bailouts while millions of homeowners either lost their homes or got stuck underwater, owing much more on their mortgage than their home was worth.

Even as the real estate market begins to recover, the mortgage crisis has left its mark. Mortgage underwriting—the criteria banks use to determine whether to make a loan—is more stringent. That’s not to say that young couples or other first-time home buyers will have a difficult time getting a mortgage. But it means that proving to the bank that you’re financially prepared for a mortgage is more important than ever, and that’s where IFS can help you today!

Contact us at the IFS office nearest to you or submit a business inquiry online.

You helped my family professionally twice and I am very pleased with your work ethic. Our experience at IFS was great! Thanks guys!

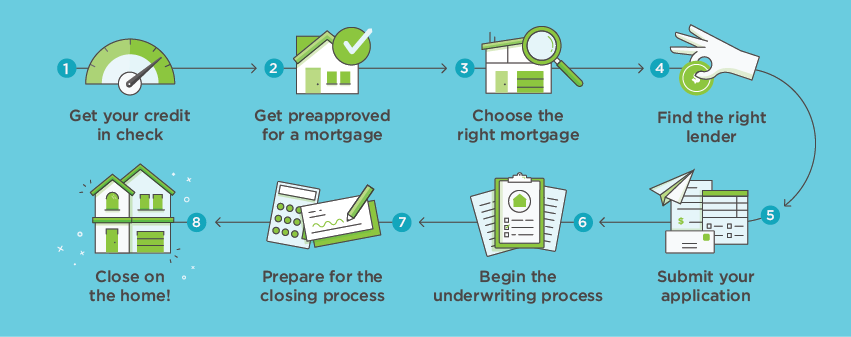

Step by Step Guide To Getting a Mortgage With Us

1.) Get Your Credit In Check

Before you set off to get a mortgage, make sure you’re financially prepared for homeownership. Do you have a lot of debt? Do you have plenty saved for a down payment? What about closing costs? If the answer to any of these questions is “No”, don’t worry it doesn’t mean a mortgage is out of your reach!

Ask yourself “how much house can I afford?” before you go further.

Additionally, know that we look closely at your credit score when determining your eligibility for a mortgage loan. Check your credit score and do anything you can to improve it, such as lowering outstanding debt, disputing any errors and holding off on applying for any other loans or credit cards. If necessary, speak with an IFS credit specialist to see what options are available to you. Once you’ve thoroughly assessed your finances and gotten your credit in shape, you’re ready to research and choose the best mortgage type for you.

2.) Get Pre-Approved

After you’ve checked your credit, getting preapproved for a mortgage will tell you how much we can assist you in borrowing for a home. Once you have your price range, you’re ready to look at houses. Getting preapproved also gives you a leg up when you start looking, because it shows sellers that you can make a solid offer up to a specific price.

Once you’re ready to apply for the loan, the process will go a little quicker since you’ve started the ball rolling with paperwork and a credit check. While pre-approval isn’t a necessary step in the mortgage process, it can save you time and money in the long run!

3.) Choose the Right Mortgage

The most important factors in determining which type of mortgage is best for you include:

- Conventional or government-backed loan: Government-backed loans, such as Federal Housing Administration loans, can make it easier for you to buy a home if your credit score isn’t great or if you don’t have money for a big down payment. Conventional loans come from banks, credit unions or online lenders, and usually require larger down payments than government-backed loans. If saving up a down payment is difficult, we can help you find assistance programs in your state.

- Fixed or adjustable rate: Fixed-rate mortgages tend to be safer because the mortgage interest rate won’t change over the life of the loan, but adjustable-rate mortgages can yield savings in some situations.

- Mortgage term: Do you want a 10-year, 20-year or 30-year mortgage? With a 30-year term, your monthly payments probably will be smaller, but you’ll pay more interest over the life of the loan.

- Know your annual percentage rate, or APR. This likely will be higher than the quoted interest rate because the APR includes all the associated costs such as origination fees and points. We’ll get into points later.

- Don’t borrow more than you can handle. IFS mortgage advisors can review amortization schedules with you to see what works best.

4.) Choose the Right Lender

Just like you want to get the home that best suits your needs, you’ll want to find a lender that best suits you and this is where Infinite Financial Services shines for you and your mortgage. If you shopped around before getting preapproved, you’re already one step ahead and will quickly see the difference in moving forward with IFS as your broker:

- We make sure your needs and financial situation are aligned with your lender choice

- We regularly communicate with you and your real estate agent

- We compare at least three lenders, ask about and uncover all fees and down payment requirements.

- We check current mortgage rates to get the best deal

- Most importantly, we get you approved!

5.) Submit Your Application

You’ll have to submit your most recent financial information along with additional documentation. Here’s the information you’ll need:

- W-2 forms from the past two years

- Pay stubs from the past 30 days

- Federal tax returns from the past two years

- Proof of other sources of income

- Recent bank statements

- Details on long-term debts such as car or student loans

- ID and Social Security number

There may be other kinds of documentation required, depending on the type of mortgage you’re getting. An IFS mortgage consultant will walk you through the process and collect the documents required for the type of mortgage we have identified.

If you’re self-employed, you’ll have to provide extra proof of your financial stability, including having a higher credit score or large cash reserves, and possibly providing business tax returns. IFS specializes in helping you through these extra requirements and has more success than any other broker in getting self-employed individuals the loans they deserve.

Within three days of receiving your application, we will give you a loan estimate, which includes:

- How much the loan will cost

- Associated fees and closing costs

- Interest rate, and possibly information on obtaining a rate lock

What’s next? Keep an eye on mortgage interest rates. If they start going up, you may want to lock your rate quickly.

6.) Begin the Underwriting Process

This part can be the most nerve-wracking, even if you’ve been preapproved. It’s more waiting, this time to get officially approved for the loan.

During the underwriting process, we help determine whether you’re eligible for the loan. Factors evaluated include:

- Credit and job history

- Debt-to-income ratio

- Current debt obligations

IFS will then order a property appraisal and credit report. An appraisal tells us the market value of your home, which it matches against the loan amount to see if what you’re asking for makes sense. If for some reason the amount you need is higher than the appraisal, don’t worry not all is lost! We can still get you approved!

Meanwhile, a home inspection will be scheduled, which will look for any defects in the home. Then you may negotiate repairs or a lower sale price before closing.

During the underwriting process, you’ll want to avoid making changes such as switching jobs or taking out another line of credit. Also avoid large purchases that increase your debt. Increasing your debt can lower your credit score, which could make the loan more costly in the end.

7.) Prepare for Closing

Finally, your loan is approved. But you’ve got a few more steps to take before the process is complete.

- Decide if you should get discount points. Do you want to pay an upfront fee — known as points — to lower your interest rate? This could be a good option if you plan on staying in your home for at least seven years.

- Purchase homeowners insurance. We will require you to do this. Shop around for the best policies. If you don’t have insurance by closing, an IFS advisor can recommend some options for you and your new home.

- Buy a title policy. And while it’s not required, it’s wise to also purchase owner’s title insurance. Both policies protect you in case there are problems with the title to the property down the road.

- Do a final walk-through of the home. Make sure nothing has changed — and the agreed-upon repairs have been made — since the home inspection.

- Receive a closing disclosure.You’ll get this three days before the scheduled closing date, which lists all the closing costs.

- Get a cashier’s check. This will be from your bank to cover closing costs.

8.) Close On The Home

You’re almost done! Here’s how the last step usually unfolds.

New mortgage closing rules set up by the Consumer Financial Protection Bureau might extend the closing process with the intention of simplifying all the paperwork before closing and avoiding any surprises.

Typically, you’ll pay between 2% and 5% of the home’s purchase price in closing costs. An IFS advisor can assist you in estimating and finalizing the closing costs.

If your mortgage down payment is less than 20% of the home’s purchase price, you will probably have to pay for private mortgage insurance. This monthly expense is typical on low-down-payment mortgages to protect involved parties in case the borrower fails to repay their loan. Once you get up to 20% equity in the home, you can take steps to cancel your PMI.

If you start having second thoughts at this point — maybe it’s all much more expensive than you thought it would be — you can still walk away. You might lose your deposit — also called earnest money — if you decide not to close. Either way, our efforts on your behalf to this point make this a rare occurrence and your IFS advisor will provide the best guidance for your circumstances regardless.

State laws will determine who’s present at closing. These people may include:

- Your lender(s)

- Your real estate agent

- A closing agent

- Your attorney

- The seller’s attorney

- A title company representative

- The seller and the seller’s agent

Don’t be afraid to ask questions throughout the process! Getting a mortgage comes with a lot of paperwork. Take the time to understand it all. Know what you’re signing and what you’re paying.

And that’s it — you made it through the mortgage obstacle course, and the loan is yours. It’s finally time to move into your new home and we at IFS couldn’t be happier than to now call you another satisfied homeowner!